The Business Succession Relief (BSR) in Dutch gift and inheritance tax is one of the most valuable tax facilities available to entrepreneurs and their families. Provided all conditions are met, up to 100% of the value of business assets can be exempt from gift or inheritance tax. But what if the ownership structure changed in the years prior to the transfer — for example, through a forced demerger (ruziesplitsing)? This raises the question: does the holding period prior to the demerger still count?

On 30 January 2026, the Dutch Supreme Court issued a definitive ruling in the long-running ‘Hearing Aids and Glasses’ case. The outcome has significant implications for anyone wishing to make a gift or bequest of a business that has undergone a legal demerger in the past.

Contents

Is a business transfer on the horizon?

Has your holding company undergone a demerger or restructuring in the past? Have it assessed in good time.

Schedule a consultation

Supreme Court (Hoge Raad), 30 January 2026, Case No. 24/01608 (ECLI:NL:HR:2026:137)

The BSR in a Nutshell

The Business Succession Relief (BSR) is an exemption under the Dutch Inheritance Tax Act 1956 (Successiewet) that allows entrepreneurs to transfer their business to the next generation without an immediate, substantial tax charge. The underlying rationale is straightforward: if the tax liability arising on a business succession must be paid immediately, it could jeopardise the continuity of the enterprise. Employees and clients alike benefit from making such transfers fiscally feasible.

Two key requirements under Article 35d(1)(c) of the Inheritance Tax Act — the so-called holding conditions — must be met for the BSR to apply to gifted or bequeathed shares:

- Direct holding condition: the donor or testator must have directly held the shares for at least five years.

- Indirect holding condition: the company whose shares are transferred must have operated a qualifying business enterprise for that same five-year period.

If either condition is not satisfied, the BSR does not apply — in whole or in part. That was precisely the issue at the heart of the ‘Hearing Aids and Glasses’ case.

The Facts: ‘Hearing Aids and Glasses’

The facts of this case are complex, but worth understanding — they reflect structures that arise regularly in practice.

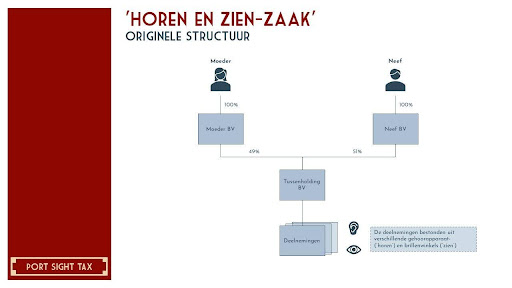

The mother of the taxpayer held, through her personal holding company (Moeder BV), an indirect 49% interest in a group holding company (Tussenholding BV). The remaining 51% was held by a nephew of the taxpayer through his own holding company (Neef BV). Tussenholding BV had several subsidiaries carrying on two types of activities: hearing aid shops (hereinafter: ‘hearing’) and opticians (hereinafter: ‘glasses’).

In 2011, a forced demerger (ruziesplitsing) took place pursuant to Article 2:334cc of the Dutch Civil Code. Under this demerger, the activities were divided: the ‘glasses’ activities were transferred to the nephew’s company, while the ‘hearing’ activities were transferred to a new subsidiary of Moeder BV; Tussenholding ‘hearing’ BV. As a result, the mother’s indirect interest in the ‘hearing’ activities increased from 49% to 100%.

.jpg)

In 2012, the ‘hearing’ activities and the business premises were further demerged into a new company (BOR BV), of which the mother held all shares. On 25 September 2013, the mother gifted all shares in BOR BV to her son (the taxpayer). The son requested the full application of the BSR to the entire value of the gift.

.jpg)

The Tax Inspector disagreed: he granted the BSR for only 49% of the value. His reasoning was that prior to the demerger, the mother was entitled to 49% of the ‘hearing’ activities. The increase of her interest to 100% as a result of the 2011 demerger triggered a new five-year holding period in respect of the additional interest (51%). Since the gift took place as early as 2013 — only two years later — the holding condition had not been satisfied for that additional interest.

The Legal Question: Does the Demerger Reset the Clock?

The case turns on one central question: does an increase in an indirect interest in a qualifying business enterprise — resulting from a forced demerger under which part of the enterprise passes entirely to the donor — trigger a new five-year period for the indirect holding condition?

The answer to that question depends on a preliminary issue: were ‘hearing’ and ‘glasses’ one or two qualifying business enterprises prior to the demerger?

- One qualifying enterprise: The mother had operated the ‘hearing’ enterprise at 49% from the outset; the demerger is merely a reorganisation whereby the previously held interest takes on a different legal form. No new period begins, and the son may claim the BSR over 100% of the value.

- Two qualifying enterprises: Prior to the demerger the mother was entitled to 49% of two separate enterprises. As a result of the demerger, she acquired an extension of her interest in ‘hearing’ (from 49% to 100%). That extension constitutes a ‘subjective increase in a qualifying enterprise’ and triggers a new five-year holding period for the additional interest. The BSR then applies only to 49%.

The Supreme Court’s Ruling

After lengthy proceedings — from the District Court of Zeeland-West Brabant (2019), through the Court of Appeal of ’s-Hertogenbosch (2021), to the Supreme Court’s referral judgment of 21 April 2023, and subsequently the Court of Appeal of Arnhem-Leeuwarden (2024) — the Supreme Court issued its definitive ruling on 30 January 2026.

The Supreme Court first confirmed the legal framework established in its 2023 referral judgment (para. 5.1.3):

"If the company concerned is entitled to a proportionate share of a business enterprise [...] and that entitlement is extended, a new, separate indirect holding period commences to that extent."

In other words: when a company increases its proportionate interest in a qualifying business enterprise, a new five-year period begins in respect of the extended portion. This applies even where the extension results from a forced demerger.

The referring court (Court of Appeal Arnhem-Leeuwarden) had established that there were two qualifying business enterprises — ‘hearing’ and ‘glasses’ — prior to the demerger. The son failed to demonstrate that they constituted a single enterprise. The Supreme Court upheld this factual finding: it disclosed no error of law and was adequately reasoned.

The consequence is that the son can invoke the BSR only in respect of 49%. The BSR does not apply to the additional interest acquired as a result of the demerger, because the five-year holding period for that portion had restarted and had not been completed at the time of the gift.

The son also invoked Article 9(2) of the Gift and Inheritance Tax Implementation Decree (URSE). That provision offers a concession for situations where the gifted shares relate to more than one enterprise. The Supreme Court dismissed this argument swiftly: the Article 9 URSE concession applies exclusively to the direct holding condition and not to the indirect holding condition. The provision applies to shares held by a natural person, not to the situation where a legal entity (the company) operates a business enterprise.

Finally, the Supreme Court confirmed that the burden of proof lies with the taxpayer. The son must demonstrate that the conditions for the BSR are satisfied; that is a prerequisite for the full BSR exemption he claimed. The Inspector bears no burden of refutation.

The Supreme Court dismissed the appeal in cassation.

What Does This Mean in Practice?

This judgment has direct implications for business succession planning, particularly in cases where a legal demerger or restructuring took place in the years preceding a planned gift or bequest.

1. A Forced Demerger Can Reset the Clock

Where a forced demerger increases the indirect interest in a qualifying business enterprise — for example from 49% to 100% — a new five-year holding period begins in respect of the additionally acquired interest (51%). This applies regardless of how long the ‘original’ 49% had been held. If you are planning to gift or bequeath a business, it is essential to establish when any restructuring took place and whether the five-year period has been completed.

2. One or Two Qualifying Enterprises: It Makes All the Difference

The characterisation as one or two qualifying business enterprises is decisive for the outcome. Had ‘hearing’ and ‘glasses’ been treated as a single integrated enterprise, the son would have been fully entitled to the BSR — since there would have been no increase in the entitlement to a business enterprise, merely a reorganisation. The distinction is not always straightforward and requires sound factual substantiation.

3. The Burden of Proof Lies with the Taxpayer: Document Everything

The Supreme Court confirms that the taxpayer must demonstrate that the conditions for the BSR are satisfied. In this case, the son partly lost because he failed to make it plausible that there was a single enterprise. The commentary on Advocate General Wattel’s opinion puts it aptly: this is a lesson for practice. Keep better records in minutes and similar documents.

Think of: resolutions from shareholders’ meetings, management reports demonstrating unified control, consolidated financial statements, shared customer databases or central procurement, and other documents substantiating the economic coherence of the activities. Documents created only after the fact carry considerably less weight.

4. Article 9(2) URSE Offers No Relief for the Indirect Holding Condition

The concession under Article 9(2) URSE — which enables holding periods to be aggregated across multiple enterprises — applies exclusively to the direct holding condition. The Supreme Court makes clear that this provision does not apply to the indirect holding condition. It is therefore a misconception to assume that this concession can provide a solution in situations such as the present one.

5. Timely Planning Is Essential

The lesson from this judgment is clear: anyone considering gifting or bequeathing a business where a restructuring has taken place in the past must verify in good time whether the BSR holding conditions have been met. Where a forced demerger has led to an increase in the interest in a qualifying business enterprise, a new five-year period must be taken into account for that additional interest. Failure to identify this in time risks a significantly higher tax charge.

In this respect, the judgment once again illustrates that the BSR is a highly technical measure, in which details — such as the characterisation of activities as one or more qualifying business enterprises, or the precise moment at which a holding period commenced — may be of decisive importance.

In Conclusion

The Supreme Court’s judgment of 30 January 2026 brings a long-running and consequential tax dispute to a close. The outcome is clear: a forced demerger that leads to an increase in the indirect interest in a qualifying business enterprise triggers a new five-year holding period for that additional interest. Anyone who does not wait out this period can only invoke the BSR in respect of the original interest.

Is a business transfer on the horizon for you or your clients, and has the holding company undergone a demerger or restructuring in the past? Make sure this is assessed in good time. The BSR offers enormous opportunities — but only if all conditions are satisfied.

Are you uncertain whether the holding conditions are met in your situation? Please contact one of our advisors.

Footnotes

- Supreme Court (Hoge Raad), 30 January 2026, Case No. 24/01608, ECLI:NL:HR:2026:137, V-N 2026/7.13.

- Supreme Court (Hoge Raad), 21 April 2023, Case No. 21/04462, ECLI:NL:HR:2023:647, BNB 2023/97.

- Opinion of Advocate General Wattel, 25 October 2024, Case No. 24/01608, ECLI:NL:PHR:2024:1114, V-N 2024/53.9.

- Court of Appeal Arnhem-Leeuwarden, 12 March 2024, Case No. BK-ARN 23/1408, ECLI:NL:GHARL:2024:1864, V-N 2024/23.1.3.

- Article 35d(1)(c) Inheritance Tax Act 1956.

- Article 9(2) Gift and Inheritance Tax Implementation Decree (text 2013).

Frequently asked questions about this topic

A forced demerger is a legal demerger in which shareholders divide their joint holdings. If this results in an increase in the indirect interest in a qualifying business enterprise, a new five-year holding period commences for the additional interest under the Business Succession Relief rules.

The five-year period for the indirect holding condition restarts from the moment the proportionate interest in a qualifying business enterprise is extended — even if this results from a restructuring or forced demerger.

The taxpayer must demonstrate that all conditions for the Business Succession Relief are satisfied. Ensure timely documentation evidencing unified control, such as shareholder resolutions, management reports, and consolidated financial statements.

Written by:

Noah Sahit

Tax Advisor

Noah Sahit is a passionate tax specialist who will further specialize in the field at Port Sight Tax. After various experiences at tax consultancy firms, Noah was the first PST member to dock his ship with our firm. This' home-grown 'tax specialist combines technical knowledge with a strong dose of Gen-Z office skills and humour.

Read more

Written by:

Noah Sahit

Tax Advisor

Noah Sahit is a passionate tax specialist who will further specialize in the field at Port Sight Tax. After various experiences at tax consultancy firms, Noah was the first PST member to dock his ship with our firm. This' home-grown 'tax specialist combines technical knowledge with a strong dose of Gen-Z office skills and humour.

Get in touch

Free Consultation

Want to know more about this topic? Book a free consultation with one of our specialists.

Book an appointment

Takes just a minute